A Guide to Divorce or Separation Finances

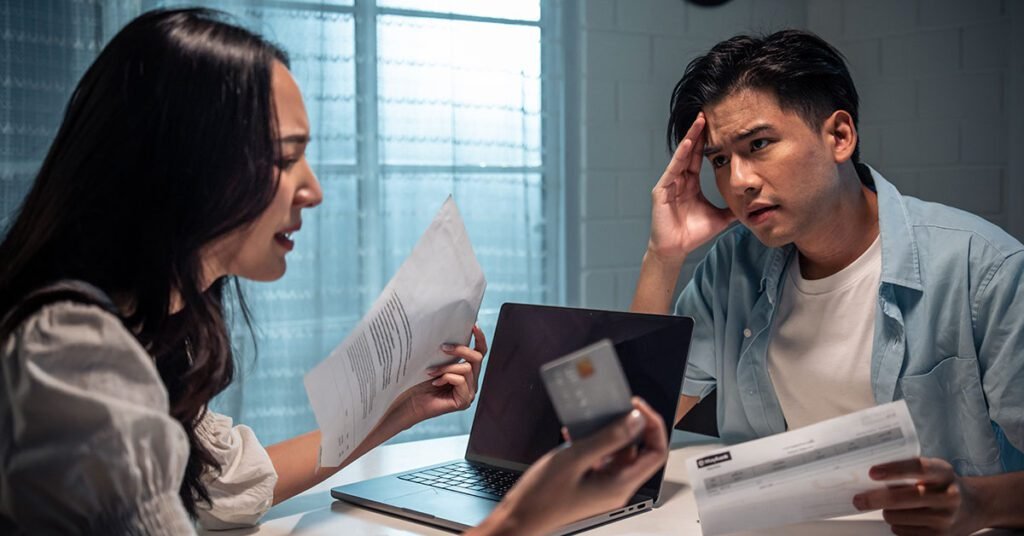

Breaking up is hard to do, especially when it comes to money matters. When you’re going through a divorce or separation, it’s like playing a twisted game of Monopoly where instead of collecting properties, you’re divvying up debts and assets.

But with a dash of practicality, we’ll navigate the tumultuous waters of managing finances during this rollercoaster ride called divorce or separation.

Divvying Up the Loot

First things first: dividing assets. It’s like deciding who gets custody of the family pet but with bank accounts and houses instead. Sit down with your soon-to-be ex and try not to resort to playing rock-paper-scissors to settle who gets what. Be fair, and remember, karma’s a boomerang, so don’t try to swipe everything for yourself.

Now comes the fun part – negotiation. It’s like haggling at a flea market, except instead of bargaining for a discount on a rug, you’re bargaining for your financial future. Be prepared to compromise, because unless you’re both fighting over the toaster, there’s bound to be some give and take.

And don’t forget about the less tangible assets, like retirement accounts and investments. These can be trickier to divide, but with a bit of creativity and a lot of patience, you can reach a fair agreement. Just remember, it’s not about who “wins” – it’s about finding a solution that allows both parties to move forward with their lives.

So let’s delve deeper into what to do once you’ve sorted through the assets.

1. Document Everything

Before you start dividing assets, it’s essential to have a clear picture of what you own and what you owe. Create a detailed inventory of all your assets, including bank accounts, real estate, vehicles, investments, and valuable possessions. Don’t forget about debts either – make a list of all outstanding loans, credit card balances, and other liabilities.

2. Seek Professional Help

Divorce or separation can be emotionally taxing, and adding financial stress to the mix can feel overwhelming. Consider enlisting the help of professionals such as lawyers, mediators, or financial advisors who specialize in divorce settlements. They can provide expert guidance and help you navigate the complexities of asset division, ensuring a fair outcome for both parties.

3. Prioritize Your Needs

When dividing assets, it’s essential to prioritize your immediate and long-term financial needs. Identify what assets are crucial for your financial stability, such as a primary residence, retirement savings, or income-generating investments. Be willing to compromise on less essential items to secure the assets that will support your future financial well-being.

4. Consider Tax Implications

Dividing assets isn’t just about who gets what – it’s also about understanding the tax implications of your decisions. Certain assets, such as retirement accounts or investment properties, may have tax consequences when transferred or sold. Consult with a tax professional to ensure you fully understand the tax implications of your asset division strategy and optimize your financial outcomes.

5. Update Your Financial Plan

With your assets divided, it’s time to update your financial plan for life post-divorce or separation. Take stock of your new financial situation, including your income, expenses, assets, and liabilities. Create a revised budget that reflects your current financial reality and sets you on a path towards financial stability and independence.

6. Protect Your Financial Future

Finally, take steps to protect your financial future. This may include updating your estate plan, updating beneficiary designations on accounts and insurance policies, and establishing a financial safety net for unexpected expenses. Remember, divorce or separation is a significant life transition, and taking proactive steps to safeguard your financial well-being is crucial.

Managing Debt Drama

Now, we’ve reached managing debt drama.

Here’s how to navigate the treacherous waters of debt management with flair:

1. Assess the Damage

First things first, take stock of the debt you’ve accumulated as a couple. This might include credit card balances, personal loans, mortgages, and any other outstanding liabilities. Lay it all out on the table (figuratively, of course) and don’t be afraid to face the cold, hard truth.

2. Divide and Conquer

Once you’ve identified your debts, it’s time to divvy them up like slices of a debt-ridden pie. Sit down with your soon-to-be ex and come up with a plan for how to allocate responsibility for each debt fairly. Maybe you take on the credit card debt while they tackle the car loan, or perhaps you split everything down the middle like a modern-day Solomon.

3. Prioritize Payoff

Not all debts are created equal, so it’s essential to prioritize which ones to tackle first. Start by focusing on high-interest debts, such as credit cards, which can quickly spiral out of control if left unchecked. Consider consolidating multiple debts into a single loan with a lower interest rate to streamline your repayment efforts and save money in the long run.

4. Communicate, Communicate, Communicate

Effective communication is key when it comes to managing debt during a divorce or separation. Keep the lines of communication open with your ex-spouse to ensure you’re both on the same page regarding debt repayment strategies and financial obligations. Remember, teamwork makes the dream work – even when it comes to paying off debt.

5. Explore Legal Options

In some cases, it may be necessary to seek legal assistance to address complex debt issues during divorce or separation. If you’re facing disputes over shared debts or concerns about financial liability, don’t hesitate to consult with a qualified attorney who can provide guidance based on your specific circumstances.

6. Focus on the Future

While managing debt during divorce or separation can feel like an uphill battle, it’s essential to keep your eyes on the prize – a brighter financial future. Stay focused on your long-term goals and make strategic decisions that will set you up for success post-divorce. With dedication and perseverance, you can conquer the debt drama and emerge stronger and more financially resilient than ever before.

I strongly suggest visiting “Managing Debt: Building a Strong Financial Foundation” for essential guidance on effectively managing debt and securing your financial future.

Planning for the Future

Planning for the future post-divorce or separation is like plotting a course through uncharted waters – it requires foresight, resilience, and maybe a compass or two. But with a sprinkle of optimism and some strategic thinking, you can steer your financial ship towards calmer seas. Here are some tips to help you chart a course for a secure financial future:

1. Set Clear Goals

Start by envisioning your ideal financial future. What do you want to accomplish?

Whether it’s buying a new home, saving for your children’s education, or building a comfortable retirement nest egg, setting clear goals will give you direction and motivation as you navigate the post-divorce landscape.

2. Create a Budget

A budget is your financial roadmap – it tells you where your money is going and how to steer it towards your goals. Take stock of your income, expenses, and savings goals, and create a budget that aligns with your priorities. Be realistic about your spending habits and look for opportunities to trim expenses and boost savings wherever possible.

I highly recommend exploring “Budgeting: Unveiling the Secrets to Financial Freedom” for invaluable insights into mastering budgeting and achieving your financial goals with confidence.

3. Build an Emergency Fund

Life is full of surprises, and having an emergency fund is like having a financial lifeboat to weather unexpected storms. Aim to set aside three to six months’ worth of living expenses in a liquid savings account to cover unforeseen expenses such as medical emergencies, car repairs, or job loss.

4. Invest Wisely

Investing is like planting seeds for your financial future – the earlier you start, the greater the harvest. Consider working with a financial advisor to develop an investment strategy that aligns with your goals, risk tolerance, and time horizon. Diversify your investment portfolio across different asset classes to spread risk and maximize potential returns.

If you’re interested in delving deeper into the world of investing, I highly recommend checking out “Investing 101: Getting Started with Investing” for essential knowledge and practical tips to kickstart your investment journey.

5. Protect Your Assets

Insurance is your financial safety net – it provides protection against unforeseen risks that could derail your financial plans. Review your insurance coverage, including health, life, disability, and property insurance, to ensure you have adequate protection for you and your loved ones.

6. Update Your Estate Planning

Divorce or separation can have significant implications for your estate plan, including wills, trusts, and beneficiary designations. Review and update your estate planning documents to reflect your current wishes and ensure your assets are distributed according to your wishes in the event of your passing.

Divorce or separation might feel like the end of the world, but it’s also a chance for a fresh start – financially and emotionally. So, grab your calculator and your sense of humor, and let’s navigate this financial rollercoaster together. Remember, laughter is the best medicine, especially when you’re drowning in a sea of paperwork and alimony payments. And who knows, maybe one day you’ll look back on this experience and laugh, preferably from the deck of your yacht bought with the settlement money.

For anyone navigating the complexities of divorce, understanding its financial ramifications is crucial. The article “Financial Implications of Divorce: Understanding the Long-Term Financial Consequence” provides an invaluable resource. It delves into the various economic challenges that can arise post-divorce, including asset division, potential impacts on retirement savings, and changes in living standards. The article also offers practical advice on financial planning and managing the long-term consequences effectively. Whether you are currently going through a divorce or just want to be informed about the possibilities, this article is a must-read. It equips you with the knowledge to make well-informed decisions that can help secure your financial future.